“Well written in a tone that alternates between serious and humorous, Wong’s timely, concise, and practical introduction is a quick and leisurely guide to modern financial literacy.” ―Booklist

Get The Book

In Get Money, personal finance expert Kristin Wong shows you the exact steps you need to take to get more money in your pocket without letting it rule your life.

“Get Money is a smart, fun, and detailed guidebook to your financial life. ―Jason Vitug, bestselling author of You Only Live Once: The Roadmap to Financial Wellness and a Purposeful Life

JOIN THE COMMUNITY

Enter here and meet your fellow money geeks.

“Kristin does the seemingly impossible: she makes learning about money a whole lot of fun. If you want to get money, get this book.” ―Liz Weston, personal finance columnist and bestselling author of Your Credit Score

Watch The Tutorials

Because sometimes you need a little visual help.

“If you want to take your financial life to the next level, you need this book!”

―J.D. Roth, founder of

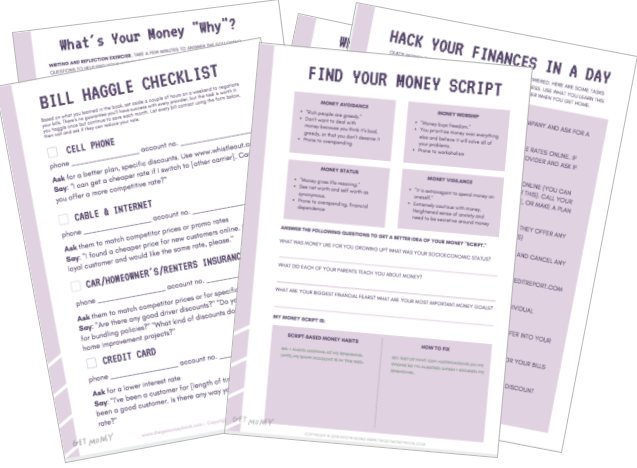

Print The Worksheets

From figuring out your budget to brainstorming your money personality, these worksheets will come in handy if you don’t want to write directly in the book (or if you want to repeat an exercise!). Hit the button below to download or print out these handy personal finance worksheets.